Fannie Mae and Freddie Mac should continue to operate as separate companies rather than merged into a single entity, and be regulated like utilities with a cap on excessive fees and prohibitions on backing risky loans.

That’s the perspective of an industry group, Community Home Lenders of America (CHLA), that represents small- and mid-sized nonbank mortgage lenders.

The CHLA this week began circulating a “sign-on letter” to Treasury Secretary Scott Bessent and Bill Pulte, the head of Fannie and Freddie’s federal regulator, the Federal Housing Finance Agency (FHFA).

The letter — prompted by reports that the Trump administration intends to take Fannie and Freddie public this year — makes a number of recommendations aimed at protecting smaller lenders, who are invited to sign it.

CHLA represents independent mortgage banks, or IMBs, which unlike traditional banks don’t accept deposits. IMBs specialize in mortgage lending, originating loans that are often bundled up into mortgage-backed securities (MBS) backed by Fannie and Freddie.

Real estate industry groups like the National Association of Realtors and the Mortgage Bankers Association have also proposed a “utility-style” model for Fannie and Freddie that would provide an explicit government guarantee while limiting the companies’ risks and profits.

During the housing bubble preceding the 2007-2009 Great Recession, Fannie and Freddie provided preferential pricing to “reckless lenders like Countrywide and WaMu,” CHLA said.

A 2021 policy amendment that mandated “G fee parity” ensures that Fannie and Freddie don’t charge smaller lenders higher guarantee fees and should be retained if the companies are released from conservatorship, the CHLA maintains.

The CHLA also urged Bessent and Pulte not to combine Fannie and Freddie into a single company with a “market monopoly.”

Fannie Mae was created as a government agency in 1938, and reorganized in 1968 as a publicly-traded, shareholder owned company. Freddie Mac was formed in 1970 to compete with it. While Fannie Mae remains the bigger company in terms of net worth and total mortgage guarantees, last year Freddie Mac backed more purchase loans ($286 billion) than its older sibling ($270 billion).

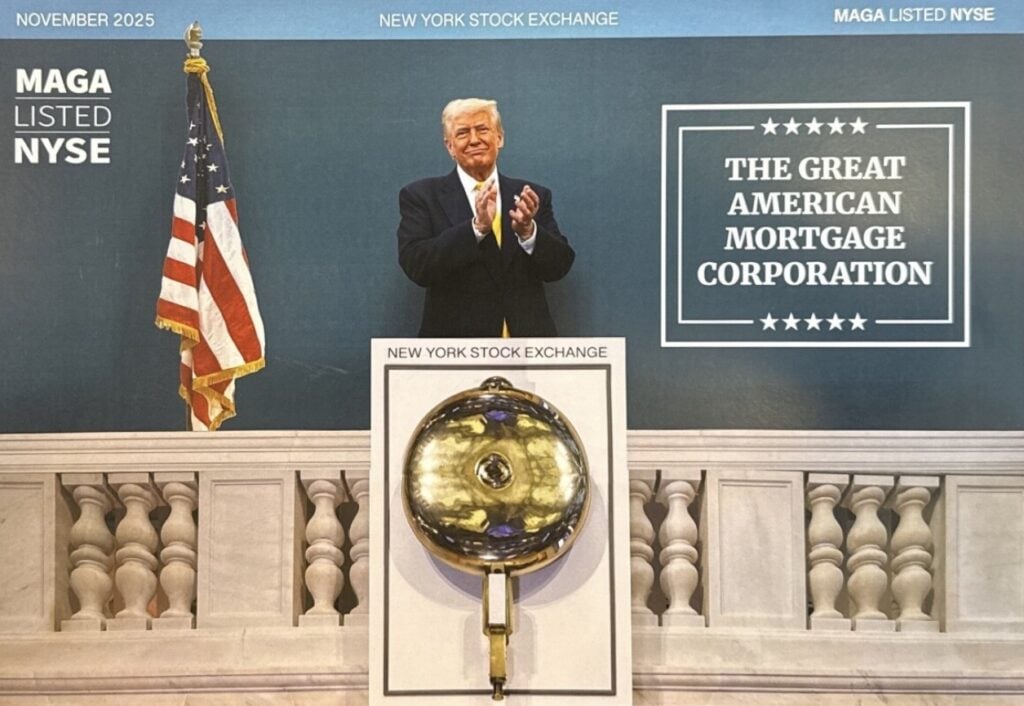

President Trump on Aug. 9 posted an imaginary image on Truth Social depicting him ringing the bell of the New York Stock Exchange for “The Great American Mortgage Corporation,” sparking speculation that the administration plans to merge Fannie and Freddie and take them public.

Pulte has posted “The Great American Mortgage Corporation” logo on more than one occasion on X.

The FHFA and the Treasury Department did not respond to Inman’s requests for comment on the CHLA’s recommendations to Pulte and Bessent.

An FHFA spokesperson said in a statement to Inman in June that the agency is “studying how, if the President elects to take Fannie and Freddie public, it can be done in the safest and soundest manner, which includes keeping them in conservatorship. In any scenario, we will ensure the MBS [mortgage-backed securities] market is safe and sound and that there is no upward pressure on rates.”

The CHLA also wants assurances that Fannie and Freddie will continue to provide “mission-based” mortgage products for condominiums, second homes and investor properties, manufactured homes and homes in rural areas.

“Stockholder earnings pressure after [Fannie and Freddie] exit from conservatorship could create incentives for [the companies] to abandon critical lower-volume mortgage products due to lower loan revenue potential,” the group warned.

Since Fannie and Freddie were placed in government conservatorship in 2008, it’s been assumed that reprivatizing the companies would entail releasing them from conservatorship.

But Bessent and Pulte have suggested that rather than releasing Fannie and Freddie from conservatorship, the government might retain an ownership stake when it takes them public, and sweep its share of their profits into a U.S. sovereign wealth fund.

“Interestingly, the President has not said anything that he wants to end conservatorship,” Pulte said in May. “We’re studying actually, potentially keeping it in conservatorship and taking it public.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter