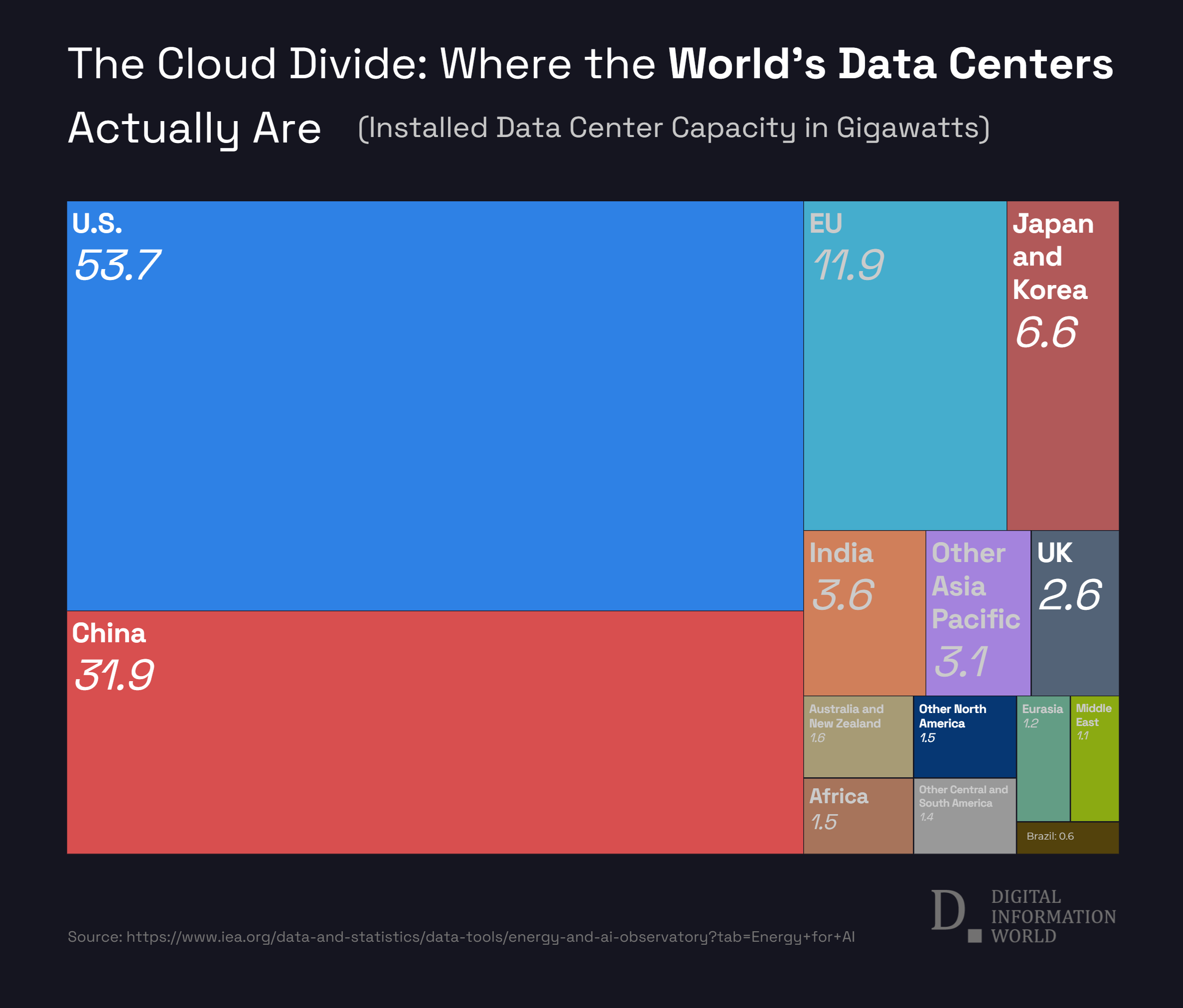

Data centers are no longer just background infrastructure. In 2024, they became central to the world’s AI ambitions, expanding at a pace few regions can match. Global capacity hit 122.2 gigawatts this year. Almost three-quarters of that total is held by just two countries.

The United States leads by far. With 53.7 gigawatts already in operation, it alone holds nearly 44 percent of the world’s total. China isn’t far behind in scale, sitting at 31.9 gigawatts. Together, they dominate the current space. The European Union, in comparison, reports 11.9 gigawatts, far lower, but still third on the global list.

Elsewhere, infrastructure remains scattered and less developed. Japan and South Korea have 6.6 combined. India’s total stands at 3.6. Most other regions, like Africa, South America, or the Middle East, show less than two. Some, including Brazil and Eurasia, are barely visible in capacity rankings.

Big Cloud Keeps Building

The growth has come mostly from the same few players. Amazon. Google. Microsoft. These firms keep pouring billions into new sites, building the backbone for cloud-based AI training. Demand from models keeps rising, so the systems behind them have had to scale.

But that pace isn’t without strain. In the U.S., some areas can’t keep up. Northern Virginia, home to the world’s busiest data center cluster, is now facing power shortages. New facilities planned through 2028 are already reserved. Space isn’t the issue. Electricity is.

China’s Capacity, Underused

China’s network has grown almost as fast as America’s. Yet much of its new infrastructure still sits idle. Reports suggest up to 80 percent of recently added capacity hasn’t been activated. The systems exist, but workloads haven’t filled them yet. There’s no single reason. Sometimes it’s power. Other times it’s demand. In many cases, it’s just timing.

Still, investment hasn’t slowed. Backers continue to push forward, betting that usage will catch up.

Europe’s Next Phase

Europe hasn’t built at the same rate, but that may be changing. Electricity demand from data centers across the continent is expected to rise 150 percent by 2035. The cause? New funding tied to AI development, estimated near $231 billion. Much of it is aimed at increasing regional capacity, with targets that could triple the EU’s footprint before 2032.

The gap remains, though. Even with those goals, the region is still well behind its American and Chinese counterparts.

The Divide Is Clear

This isn’t a balanced map. Most of the infrastructure sits in just a few places. Others are years behind or still trying to begin. The spread is uneven because the growth hasn’t followed a steady pattern. It’s been led by those who could afford to move fast and build big.

That’s unlikely to shift soon. Hyperscalers still set the pace. Until smaller regions solve the problems of power, planning, and investment, most capacity will remain where it already is, clustered tightly in the hands of the few who built early and kept going.

Read next: In 2025, Americans No Longer Search the Same Way. Trust, Age, and Task Now Shape Where They Go