Millions of borrowers were dealt a bitter blow yesterday as soaring inflation shattered hopes of an interest rate cut.

Markets are now betting that rates will remain unchanged for the rest of the year after higher air fares, fuel and food prices pushed consumer price inflation to 3.8 per cent, up from 3.6 per cent in June.

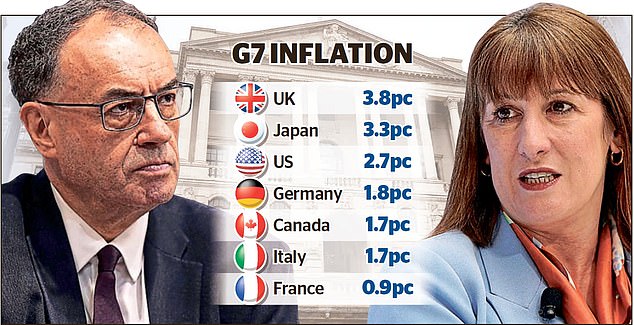

That was the highest level in 18 months and above forecasts of 3.7 per cent. It means prices in Britain are rising more quickly than anywhere else in the G7 group of advanced economies.

And it piles pressure on the Bank of England – and governor Andrew Bailey – which is tasked with keeping inflation at 2 per cent.

It is also a blow to Rachel Reeves, whose faltering stewardship of the economy has seen growth slow in recent months and unemployment rise by more than 200,000 since Labour came to power.

Experts said the Chancellor’s £25billion employer National Insurance raid, as well as a sharp increase in the minimum wage bore much of the blame for the rise in inflation as firms pass on higher costs to consumers.

Under pressure: Bank of England governor Andrew Bailey and Chancellor Rachel Reeves

The Bank has already been turning more hawkish as it voted to cut rates to 4 per cent last month by the narrowest of margins.

And it has also warned inflation will continue to rise, hitting 4 per cent by the end of this year.

Last night, market betting suggested there was a near zero chance of a rate cut next month and just a one-in-four likelihood that the BoE will reduce rates in November.

Traders also saw a 56 per cent probability of rates being held in December, meaning borrowers are likely to have to wait until February 2026 for any relief.

Fears of persistent inflation have sent UK borrowing costs higher in recent days with yields on 30-year bonds, known as gilts, rising to the highest level since 1998 earlier this week.

The sell-off in bonds – whose yields rise as prices fall – has since abated. But UK borrowing costs continue to be higher than those of other advanced economies.

Yesterday’s inflation figures are likely to have particularly concerned the Bank of England’s rate-setting Monetary Policy Committee (MPC) because of an unexpectedly big jump in services sector prices – a metric that the Bank watches closely.

Services sector inflation rose from 4.7 per cent in June to 5 per cent in July.

The Bank has been steadily cutting rates since last summer after a bout of spiralling price rises – that saw inflation hit more than 11 per cent – appeared to have been brought under control as it came down to around 2 per cent.

But it has since drifted upwards causing doubts that the Bank can continue on the same path.

Elliott Jordan-Doak, senior UK economist at Pantheon Macroeconomics, said: ‘Inflation is set to stay miles above target for the foreseeable future.

We expect headline inflation to remain above 3 per cent until April 2026, forcing the MPC to stay on hold for the rest of this year at least.’

Expectations that rates will stay higher for longer are likely to have an impact on fixed rate mortgage deals.

David Hollingworth, associate director at L&C Mortgages, said: ‘Mortgage borrowers have been enjoying a market where rates have been dropping.

‘Fixed rates have been pricing in the recent and future cuts, so have been edging down with a host of deals now below 4 per cent.

‘Those reductions have tended to come in small increments, but we could see that slow further or even reverse in some cases if the market reacts badly to the threat of higher inflation than was previously expected.’

DIY INVESTING PLATFORMS

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.

Compare the best investing account for you