Pakistan State Oil Company Limited (PSO) has announced impressive financial results for the first quarter of Fiscal Year 2026, posting a profit after tax of Rs. 9.39 billion, up 136% year-on-year from Rs. 3.97 billion recorded in the same period last year.

The company’s earnings per share (EPS) rose to Rs. 20.0, compared to Rs. 8.5 last year. According to Arif Habib Ltd (AHL) Research, the surge in profitability was driven by inventory gains, improved gross margins, and a sharp fall in finance costs.

Revenue and Margin Performance by PSO

PSO’s net revenue stood at Rs. 737.2 billion, down 6% year-on-year due to lower volumes of high-speed diesel (HSD) and furnace oil. However, sales of motor spirit (MS) grew 1% to 761,000 tons, while HSD sales rose 6% to 675,000 tons.

Average prices for MS and HSD increased by Rs. 2.9 and Rs. 7.7 per litre, respectively, compared to last year. The company’s gross profit climbed 19% to Rs. 30.05 billion, pushing gross margins to 4.1%, the highest since September 2023. The gain came mainly from inventory valuation benefits and stronger lubricant pricing.

Finance costs dropped sharply by 43% year-on-year to Rs. 5.95 billion, thanks to lower short-term borrowings and reduced interest rates. At the same time, other income jumped 40% to Rs. 4.55 billion, driven by financial charges on line-fill cost.

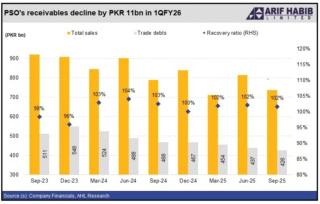

Improved Receivables and Debt Position

According to AHL Research[1], PSO’s receivables declined by Rs. 11 billion in 1QFY26, reaching Rs. 426 billion as of September 2025. Since December 2023, the company’s receivables have dropped by Rs. 122 billion, while total debt also decreased by Rs. 122 billion to Rs. 324 billion.

The company’s recovery ratio remained strong at 102%, reflecting improved cash flow and collection efficiency.

PSO booked an effective tax rate of 54.4% during the quarter, lower than 66.1% recorded last year. The company’s continued focus on margin improvement, better recoveries, and efficient cost management has significantly strengthened its financial position heading into the rest of FY26.

References

- ^ AHL Research (web.facebook.com)